Hierarchical ITS for staggered launches (event-study)#

This notebook demonstrates HierarchicalInterruptedTimeSeries, a multi-unit ITS design where each unit (e.g. a product) has its own treatment time. Per-unit intercepts, time trends, covariate slopes and the launch “lift” are partially

pooled toward shared population-level hyperparameters, so sparse units borrow strength from well-observed ones and we recover a posterior over the population effect that can be used to forecast the impact of a new launch.

The model always includes hierarchical (random) linear time trends per unit, \(\gamma_i \sim \mathcal{N}(\mu_\gamma, \sigma_\gamma)\), so that the baseline for each unit can drift over time rather than being a flat intercept. This is important for avoiding confounding between secular trends and the treatment effect.

Four effect parameterizations are available:

effect_type='instant'— a single post-launch level shift per unit.effect_type='saturation'— a Hill (logistic-type) saturation curve: the effect ramps up smoothly after launch and asymptotes at a per-unit ceiling, rather than jumping instantly to its final size.effect_type='event_study'— dynamic effects across post-launch event-time bins.effect_type='placebo'— the event-study form extended with pre-launch leads as placebos.

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import pymc as pm

import causalpy as cp

from causalpy.pymc_models import HierarchicalLaunchITS

rng = np.random.default_rng(42)

Instant lift model#

DGP: a flat post-launch step of size lift_i ~ N(12, 4). Each product’s effect is constant from the launch week onwards — the simplest causal story and the one the instant model is designed for.

TRUE_MU_LIFT = 12.0

TRUE_SIGMA_LIFT = 4.0

_lift_rng = np.random.default_rng(7)

_lift_i = _lift_rng.normal(TRUE_MU_LIFT, TRUE_SIGMA_LIFT, N_PRODUCTS)

def instant_effect(tau, i, rng):

return _lift_i[i] * (tau >= 0).astype(float)

df_instant = simulate_panel(instant_effect, seed=0)

result_instant = cp.HierarchicalInterruptedTimeSeries(

data=df_instant,

formula="sales ~ 0 + emails + price",

unit_col="product",

time_col="week_idx",

treatment_time_col="launch_week",

effect_type="instant",

seasonality={"period": 52, "K": 2},

model=HierarchicalLaunchITS(

sample_kwargs={

"draws": 1000,

"tune": 1500,

"chains": 4,

"target_accept": 0.95,

"random_seed": 42,

"progressbar": False,

}

),

)

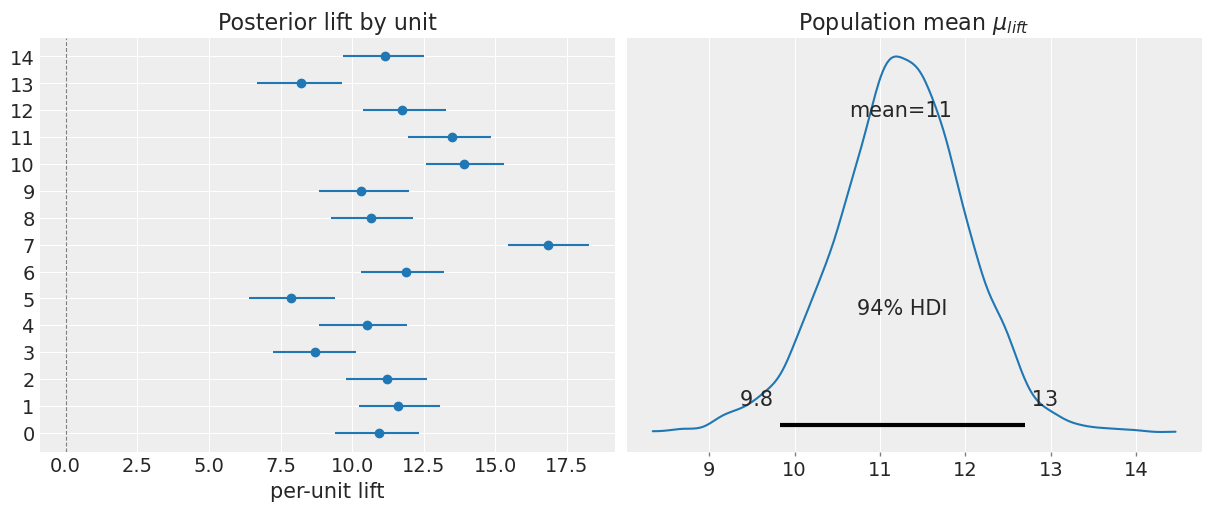

result_instant.summary()

result_instant.plot();

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [mu_alpha, sigma_alpha, z_alpha, mu_gamma, sigma_gamma, z_gamma, mu_beta, sigma_beta, z_beta, beta_season, mu_lift, sigma_lift, z_lift, sigma]

/Users/nathanielforde/mambaforge/envs/CausalPy/lib/python3.14/site-packages/pymc/step_methods/hmc/quadpotential.py:316: RuntimeWarning: overflow encountered in dot

return 0.5 * np.dot(x, v_out)

Sampling 4 chains for 1_500 tune and 1_000 draw iterations (6_000 + 4_000 draws total) took 128 seconds.

The rhat statistic is larger than 1.01 for some parameters. This indicates problems during sampling. See https://arxiv.org/abs/1903.08008 for details

The effective sample size per chain is smaller than 100 for some parameters. A higher number is needed for reliable rhat and ess computation. See https://arxiv.org/abs/1903.08008 for details

Sampling: [beta_season, mu_alpha, mu_beta, mu_gamma, mu_lift, sigma, sigma_alpha, sigma_beta, sigma_gamma, sigma_lift, y_hat, z_alpha, z_beta, z_gamma, z_lift]

Sampling: [y_hat]

Sampling: [y_hat]

Sampling: [y_hat]

Hierarchical ITS (launch / event-study)

Formula: sales ~ 0 + emails + price

Effect type: instant

Units: 15

E[mu_lift] = 11.2 E[sigma_lift] = 2.61

Inspecting the fitted model#

Every fitted HierarchicalInterruptedTimeSeries exposes the full PyMC posterior via result.idata (an ArviZ InferenceData object). From here you can visualise the model graph, check convergence, extract effect summaries, and compute Bayesian R².

# The model DAG — shows all hierarchical parameters and their dependencies

pm.model_to_graphviz(result_instant.model)

import arviz as az

# Convergence diagnostics for key hyperparameters: R-hat near 1.0 and

# large ESS (effective sample size) indicate healthy sampling.

az.summary(

result_instant.idata,

var_names=["mu_lift", "sigma_lift", "mu_gamma", "sigma_gamma", "sigma"],

)

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| mu_lift | 11.240 | 0.766 | 9.831 | 12.698 | 0.028 | 0.017 | 776.0 | 1410.0 | 1.0 |

| sigma_lift | 2.612 | 0.584 | 1.623 | 3.670 | 0.017 | 0.014 | 1201.0 | 2026.0 | 1.0 |

| mu_gamma | 0.734 | 0.166 | 0.437 | 1.064 | 0.003 | 0.003 | 2949.0 | 2338.0 | 1.0 |

| sigma_gamma | 0.313 | 0.195 | 0.001 | 0.632 | 0.007 | 0.003 | 767.0 | 1001.0 | 1.0 |

| sigma | 3.974 | 0.052 | 3.882 | 4.073 | 0.001 | 0.001 | 6222.0 | 2970.0 | 1.0 |

# effect_summary() returns an EffectSummary with a .table (DataFrame) and

# .text (prose). The table reports posterior mean, HDI, and the probability

# that the effect is positive — a quick decision-making summary.

es = result_instant.effect_summary()

display(es.table)

print(es.text)

| mean | hdi_95_low | hdi_95_high | prob_positive | |

|---|---|---|---|---|

| parameter | ||||

| mu_lift | 11.240289 | 9.649514 | 12.674919 | 1.0 |

| sigma_lift | 2.612079 | 1.709416 | 3.972569 | 1.0 |

Post-period: Hierarchical ITS (launch / event-study)

Effect type: instant

Units: 15

# Bayesian R² — how much variance in the outcome is explained by the model.

result_instant.score

unit_0_r2 0.892759

unit_0_r2_std 0.001286

dtype: float64

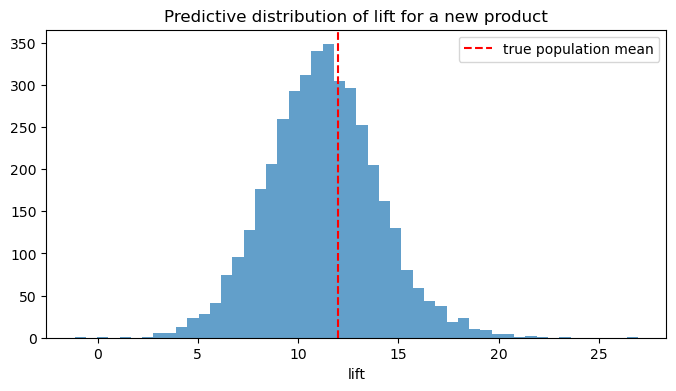

Predictive distribution for a new launch#

Because the model has a posterior over the population hyperparameters, we can sample the lift we would expect from a yet-unobserved product.

new_lift = result_instant.predictive_for_new_unit(size=4000, random_seed=0)

fig, ax = plt.subplots(figsize=(8, 4))

ax.hist(new_lift, bins=50, alpha=0.7)

ax.axvline(TRUE_MU_LIFT, color="red", ls="--", label="true population mean")

ax.set_title("Predictive distribution of lift for a new product")

ax.set_xlabel("lift")

ax.legend()

plt.show()

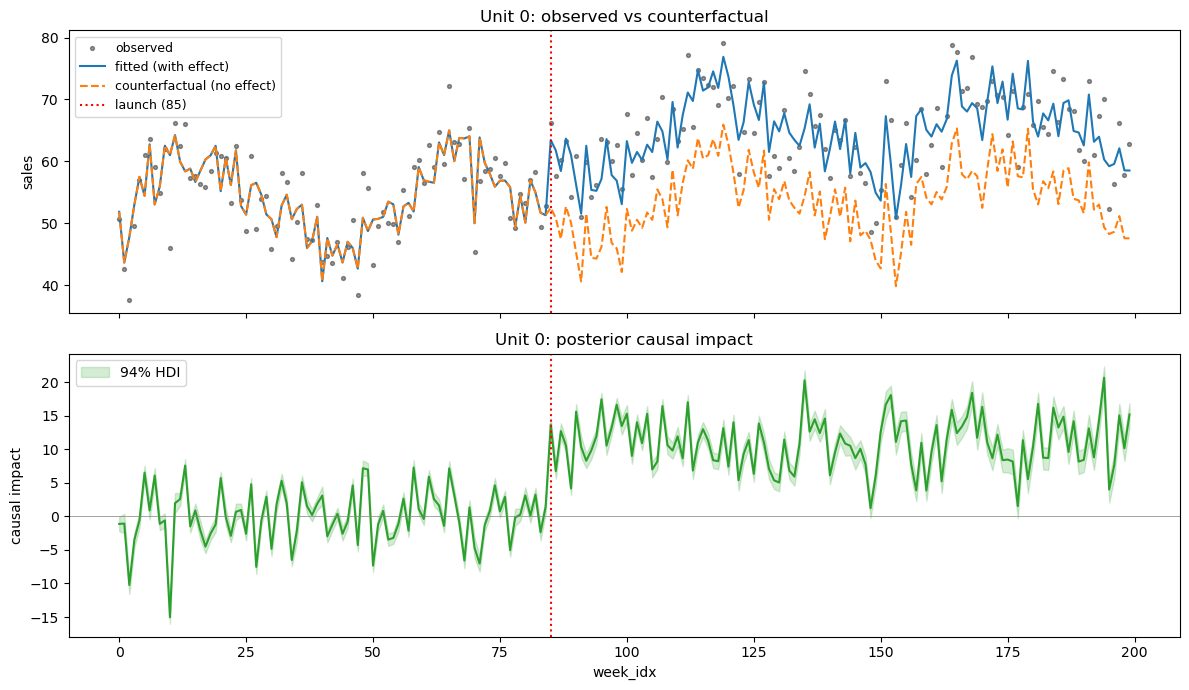

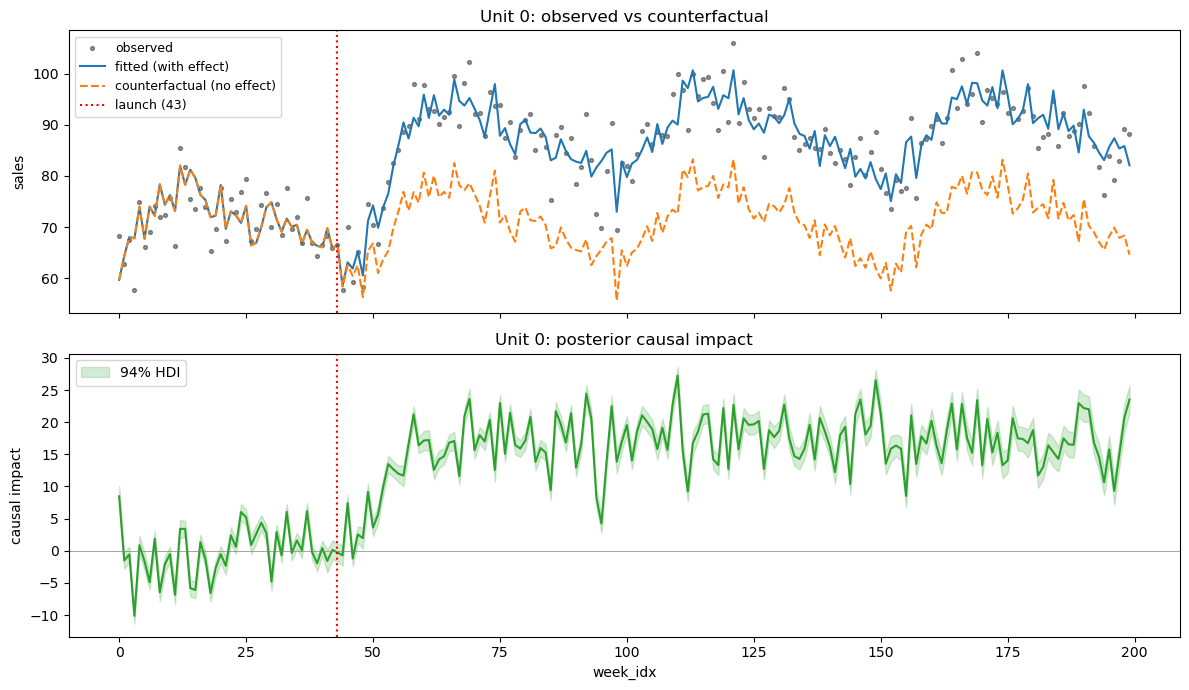

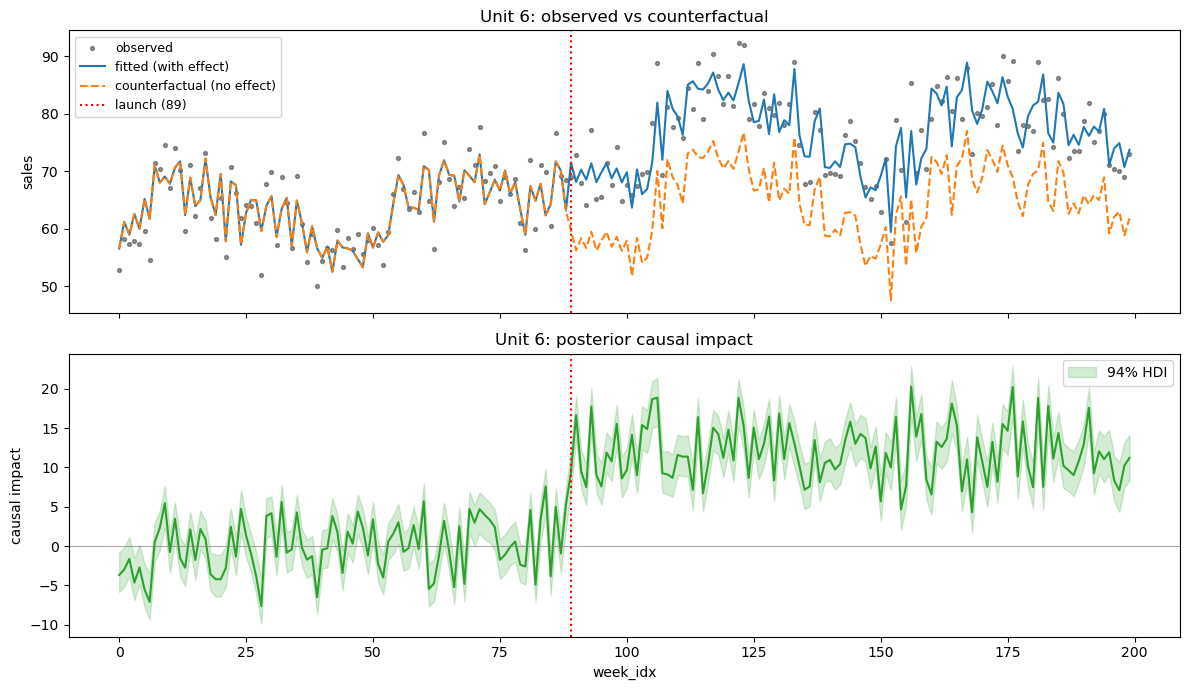

Observed vs counterfactual (single unit)#

The fitted experiment stores three key objects for causal reasoning:

result.observed_pred— posterior predictive under the actual design (with treatment effect switched on).result.counterfactual_pred— posterior predictive under the counterfactual design (treatment effect zeroed out — what would have happened without launch).result.impact—observed - counterfactual, the unit-level posterior of the causal effect at every time point.

The plot_unit() method visualises all three for a single product.

result_instant.plot_unit(unit_id=0)

plt.show()

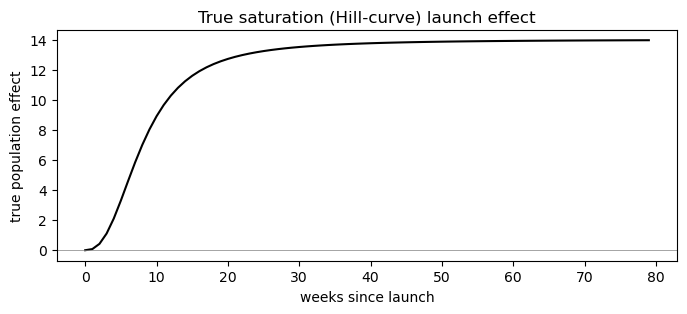

Saturation (Hill-curve) model#

DGP: rather than an instant step, the true effect follows a Hill (logistic-type) saturation curve in event time — it ramps up smoothly after launch and asymptotes at a per-unit ceiling L_i, reaching half of that ceiling after k_i weeks:

This is the same functional form used for diminishing-returns / adstock saturation in media-mix models — here the “dose” is simply time-since-launch. It’s a much closer description of how adoption, distribution build and awareness actually accumulate after a real launch than an instant jump. effect_type='saturation' fits L_i and k_i hierarchically per unit (log scale, non-centered); the Hill exponent s (curve sharpness) is a single shared population parameter.

def hill(x, k, s):

"""Hill (logistic-type) saturation curve, x clipped to [0, inf)."""

x = np.clip(np.asarray(x, dtype=float), 0, None)

return x**s / (k**s + x**s)

TRUE_L_MEAN = 14.0 # ceiling lift, population mean

TRUE_L_SD_LOG = 0.15 # per-unit heterogeneity (log scale)

TRUE_K_MEAN = 8.0 # half-saturation time (weeks), population mean

TRUE_K_SD_LOG = 0.15

TRUE_S = 2.5 # Hill exponent (shared across units)

_sat_rng = np.random.default_rng(13)

_L_i = np.exp(_sat_rng.normal(np.log(TRUE_L_MEAN), TRUE_L_SD_LOG, N_PRODUCTS))

_k_i = np.exp(_sat_rng.normal(np.log(TRUE_K_MEAN), TRUE_K_SD_LOG, N_PRODUCTS))

def saturation_effect(tau, i, rng):

return _L_i[i] * hill(tau, _k_i[i], TRUE_S)

df_saturation = simulate_panel(saturation_effect, seed=3)

# Show the true population saturation curve we expect to recover.

tau_grid = np.arange(0, 80)

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(tau_grid, TRUE_L_MEAN * hill(tau_grid, TRUE_K_MEAN, TRUE_S), color="black")

ax.axhline(0, color="grey", lw=0.5)

ax.set_xlabel("weeks since launch")

ax.set_ylabel("true population effect")

ax.set_title("True saturation (Hill-curve) launch effect")

plt.show()

result_saturation = cp.HierarchicalInterruptedTimeSeries(

data=df_saturation,

formula="sales ~ 0 + emails + price",

unit_col="product",

time_col="week_idx",

treatment_time_col="launch_week",

effect_type="saturation",

seasonality={"period": 52, "K": 2},

model=HierarchicalLaunchITS(

sample_kwargs={

"draws": 1000,

"tune": 1500,

"chains": 4,

"target_accept": 0.95,

"random_seed": 42,

"progressbar": False,

}

),

)

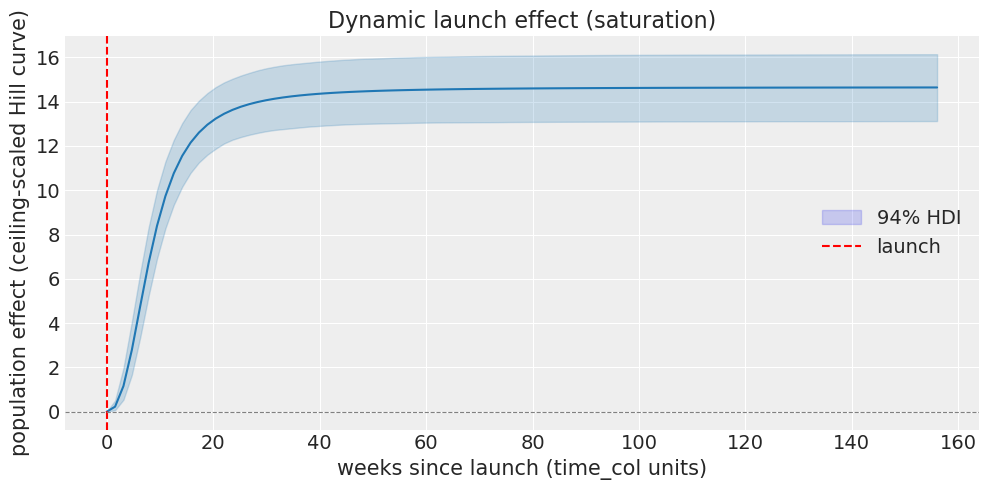

result_saturation.summary()

result_saturation.plot();

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [mu_alpha, sigma_alpha, z_alpha, mu_gamma, sigma_gamma, z_gamma, mu_beta, sigma_beta, z_beta, beta_season, mu_logL, sigma_logL, z_logL, mu_logk, sigma_logk, z_logk, s, sigma]

/Users/nathanielforde/mambaforge/envs/CausalPy/lib/python3.14/site-packages/pymc/step_methods/hmc/quadpotential.py:316: RuntimeWarning: overflow encountered in dot

return 0.5 * np.dot(x, v_out)

Sampling 4 chains for 1_500 tune and 1_000 draw iterations (6_000 + 4_000 draws total) took 327 seconds.

The rhat statistic is larger than 1.01 for some parameters. This indicates problems during sampling. See https://arxiv.org/abs/1903.08008 for details

The effective sample size per chain is smaller than 100 for some parameters. A higher number is needed for reliable rhat and ess computation. See https://arxiv.org/abs/1903.08008 for details

Sampling: [beta_season, mu_alpha, mu_beta, mu_gamma, mu_logL, mu_logk, s, sigma, sigma_alpha, sigma_beta, sigma_gamma, sigma_logL, sigma_logk, y_hat, z_alpha, z_beta, z_gamma, z_logL, z_logk]

Sampling: [y_hat]

Sampling: [y_hat]

Sampling: [y_hat]

Hierarchical ITS (launch / event-study)

Formula: sales ~ 0 + emails + price

Effect type: saturation

Units: 15

E[L] (ceiling lift) = 14.7 E[k] (half-saturation time) = 8.43 E[s] (Hill exponent) = 2.55

/Users/nathanielforde/Documents/Github/CausalPy/causalpy/experiments/hierarchical_interrupted_time_series.py:621: UserWarning: The figure layout has changed to tight

fig.tight_layout()

Convergence diagnostics and effect summary#

L and k are fit hierarchically on the log scale (mu_logL/sigma_logL, mu_logk/sigma_logk); s is a single shared parameter. effect_summary() reports the population-level ceiling lift, half-saturation time and Hill exponent on their natural (exponentiated) scale.

# R-hat near 1.0 and large ESS indicate healthy sampling.

display(

az.summary(

result_saturation.idata,

var_names=[

"mu_logL",

"sigma_logL",

"mu_logk",

"sigma_logk",

"s",

"mu_gamma",

"sigma_gamma",

"sigma",

],

)

)

es = result_saturation.effect_summary()

display(es.table)

print(es.text)

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| mu_logL | 2.683 | 0.056 | 2.573 | 2.780 | 0.002 | 0.001 | 1190.0 | 2143.0 | 1.0 |

| sigma_logL | 0.177 | 0.046 | 0.097 | 0.260 | 0.001 | 0.001 | 1535.0 | 1918.0 | 1.0 |

| mu_logk | 2.129 | 0.077 | 1.982 | 2.270 | 0.001 | 0.001 | 2859.0 | 3028.0 | 1.0 |

| sigma_logk | 0.233 | 0.074 | 0.100 | 0.365 | 0.002 | 0.001 | 1577.0 | 2572.0 | 1.0 |

| s | 2.553 | 0.269 | 2.061 | 3.078 | 0.004 | 0.004 | 5773.0 | 3226.0 | 1.0 |

| mu_gamma | 0.634 | 0.210 | 0.252 | 1.045 | 0.003 | 0.003 | 3850.0 | 3084.0 | 1.0 |

| sigma_gamma | 0.302 | 0.211 | 0.000 | 0.677 | 0.006 | 0.004 | 1026.0 | 1676.0 | 1.0 |

| sigma | 4.099 | 0.054 | 3.997 | 4.200 | 0.001 | 0.001 | 8317.0 | 2920.0 | 1.0 |

| mean | hdi_95_low | hdi_95_high | prob_positive | |

|---|---|---|---|---|

| parameter | ||||

| L (ceiling lift) | 14.650835 | 13.077124 | 16.244950 | 1.0 |

| k (half-saturation time) | 8.433520 | 7.217934 | 9.774802 | 1.0 |

| s (Hill exponent) | 2.553101 | 2.071411 | 3.148848 | 1.0 |

Post-period: Hierarchical ITS (launch / event-study)

Effect type: saturation

Units: 15

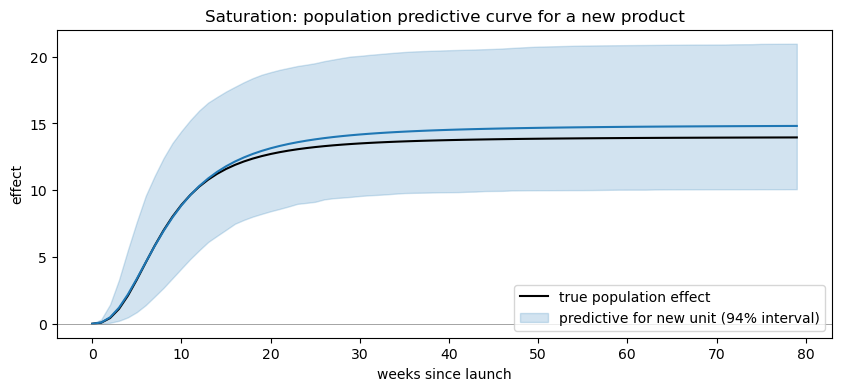

Population predictive curve for a new unit#

For effect_type='saturation', predictive_for_new_unit returns a (draws, 3) array of [L, k, s] samples for a hypothetical new product. Turning each draw into a full Hill curve and overlaying the resulting predictive band on the true population curve shows how well the model recovers both how big (L) and how fast (k) the effect is.

new_sat = result_saturation.predictive_for_new_unit(size=4000, random_seed=0)

# new_sat shape: (4000, 3) -> columns [L, k, s]

tau_grid = np.arange(0, 80)

L_draws, k_draws, s_draws = new_sat[:, 0], new_sat[:, 1], new_sat[:, 2]

curves = L_draws[:, None] * hill(tau_grid[None, :], k_draws[:, None], s_draws[:, None])

pred_mean = curves.mean(axis=0)

pred_lo = np.percentile(curves, 3, axis=0)

pred_hi = np.percentile(curves, 97, axis=0)

fig, ax = plt.subplots(figsize=(10, 4))

ax.plot(

tau_grid,

TRUE_L_MEAN * hill(tau_grid, TRUE_K_MEAN, TRUE_S),

color="black",

label="true population effect",

)

ax.fill_between(

tau_grid,

pred_lo,

pred_hi,

color="C0",

alpha=0.2,

label="predictive for new unit (94% interval)",

)

ax.plot(tau_grid, pred_mean, color="C0")

ax.axhline(0, color="grey", lw=0.5)

ax.set_xlabel("weeks since launch")

ax.set_ylabel("effect")

ax.set_title("Saturation: population predictive curve for a new product")

ax.legend()

plt.show()

Observed vs counterfactual (single unit)#

Same three objects as the instant model (observed_pred, counterfactual_pred, impact) — but now the counterfactual gap traces out the shape of the Hill curve, ramping up after launch, rather than jumping instantly to a constant lift.

result_saturation.plot_unit(unit_id=0)

plt.show()

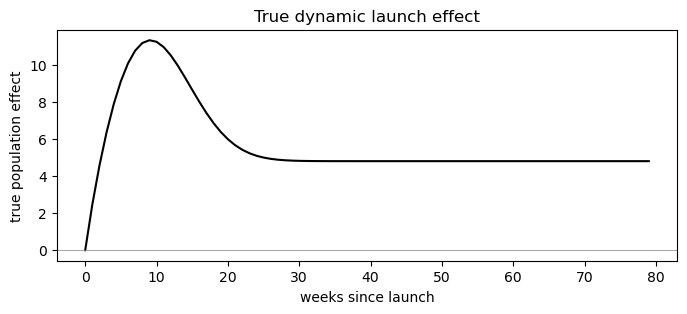

Event-study (dynamic) model#

DGP: a realistic launch curve — awareness ramps up over the first few weeks, peaks around week 8, then decays toward a lower long-run level as novelty wears off. A single “instant” lift would average this over time and miss the story entirely; the event-study variant estimates a separate population effect per post-launch bin and should trace out the true curve.

TRUE_MU_AMP = 12.0

TRUE_SIGMA_AMP = 3.0

_amp_rng = np.random.default_rng(11)

_amp_i = _amp_rng.normal(TRUE_MU_AMP, TRUE_SIGMA_AMP, N_PRODUCTS)

def launch_shape(tau):

"""Ramp-up, peak around week 8, decay toward ~40% long-run level."""

tau = np.asarray(tau, dtype=float)

return np.where(

tau < 0,

0.0,

(1 - np.exp(-tau / 3.0)) * (0.4 + 0.6 * np.exp(-((tau - 8.0) ** 2) / 80.0)),

)

def dynamic_effect(tau, i, rng):

return _amp_i[i] * launch_shape(tau)

df_event = simulate_panel(dynamic_effect, seed=1)

# Show the true population event-time curve we expect to recover.

tau_grid = np.arange(0, 80)

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(tau_grid, TRUE_MU_AMP * launch_shape(tau_grid), color="black")

ax.axhline(0, color="grey", lw=0.5)

ax.set_xlabel("weeks since launch")

ax.set_ylabel("true population effect")

ax.set_title("True dynamic launch effect")

plt.show()

result_event = cp.HierarchicalInterruptedTimeSeries(

data=df_event,

formula="sales ~ 0 + emails + price",

unit_col="product",

time_col="week_idx",

treatment_time_col="launch_week",

effect_type="event_study",

bin_edges=[0, 4, 8, 12, 16, 20, 26, 39, 52, 78, 10000],

seasonality={"period": 52, "K": 2},

model=HierarchicalLaunchITS(

sample_kwargs={

"draws": 1000,

"tune": 1500,

"chains": 4,

"target_accept": 0.95,

"random_seed": 42,

"progressbar": False,

}

),

)

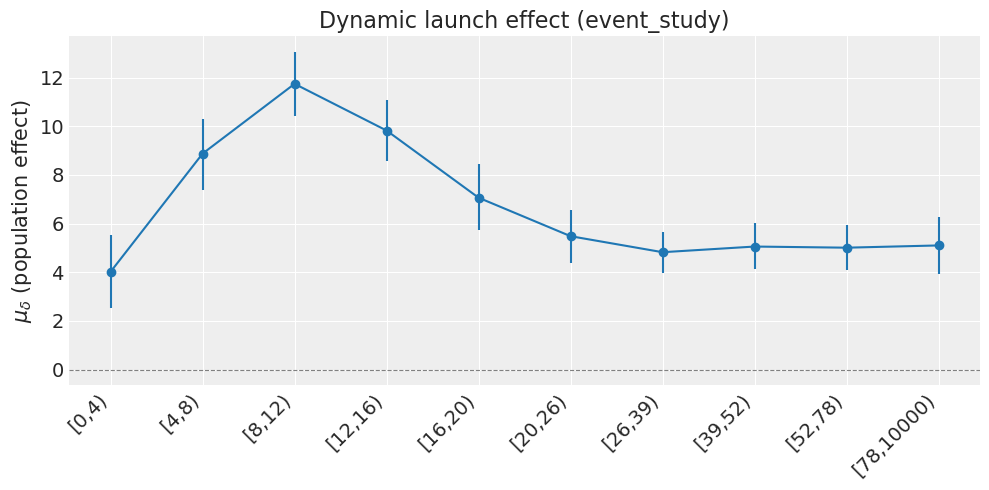

result_event.summary()

result_event.plot();

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [mu_alpha, sigma_alpha, z_alpha, mu_gamma, sigma_gamma, z_gamma, mu_beta, sigma_beta, z_beta, beta_season, mu_delta, sigma_delta, z_delta, sigma]

/Users/nathanielforde/mambaforge/envs/CausalPy/lib/python3.14/site-packages/pymc/step_methods/hmc/quadpotential.py:316: RuntimeWarning: overflow encountered in dot

return 0.5 * np.dot(x, v_out)

Sampling 4 chains for 1_500 tune and 1_000 draw iterations (6_000 + 4_000 draws total) took 221 seconds.

Sampling: [beta_season, mu_alpha, mu_beta, mu_delta, mu_gamma, sigma, sigma_alpha, sigma_beta, sigma_delta, sigma_gamma, y_hat, z_alpha, z_beta, z_delta, z_gamma]

Sampling: [y_hat]

Sampling: [y_hat]

Sampling: [y_hat]

Hierarchical ITS (launch / event-study)

Formula: sales ~ 0 + emails + price

Effect type: event_study

Units: 15

[0,4) mu_delta = +4.02

[4,8) mu_delta = +8.87

[8,12) mu_delta = +11.7

[12,16) mu_delta = +9.82

[16,20) mu_delta = +7.06

[20,26) mu_delta = +5.48

[26,39) mu_delta = +4.82

[39,52) mu_delta = +5.05

[52,78) mu_delta = +5.01

[78,10000) mu_delta = +5.1

/Users/nathanielforde/Documents/Github/CausalPy/causalpy/experiments/hierarchical_interrupted_time_series.py:668: UserWarning: The figure layout has changed to tight

fig.tight_layout()

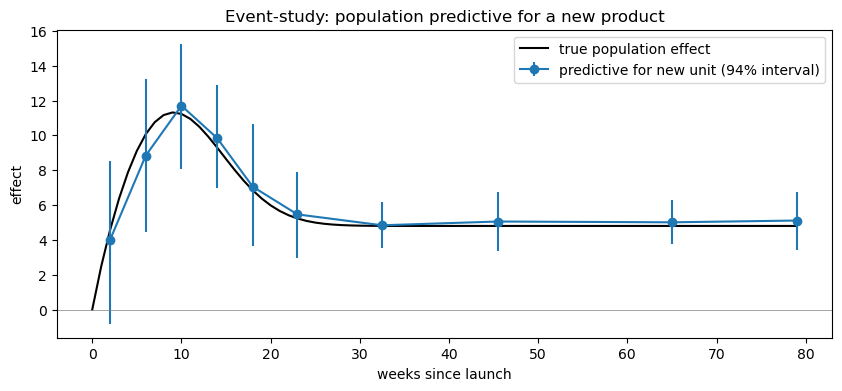

Population predictive for a new unit#

For the event-study variant, predictive_for_new_unit returns a (draws, n_bins) array — one draw from \(\mathcal{N}(\mu_\delta, \sigma_\delta)\) per bin per posterior sample. We can overlay the posterior mean and HDI on the true population curve to see how well the model recovers the dynamic launch shape.

new_delta = result_event.predictive_for_new_unit(size=4000, random_seed=0)

# new_delta shape: (4000, n_bins)

bin_edges = [0, 4, 8, 12, 16, 20, 26, 39, 52, 78, 10000]

bin_mids = [

0.5 * (bin_edges[k] + min(bin_edges[k + 1], 80)) for k in range(len(bin_edges) - 1)

]

fig, ax = plt.subplots(figsize=(10, 4))

# True curve

tau_grid = np.arange(0, 80)

ax.plot(

tau_grid,

TRUE_MU_AMP * launch_shape(tau_grid),

color="black",

label="true population effect",

)

# Posterior predictive for new unit

pred_mean = new_delta.mean(axis=0)

pred_lo = np.percentile(new_delta, 3, axis=0)

pred_hi = np.percentile(new_delta, 97, axis=0)

ax.errorbar(

bin_mids,

pred_mean,

yerr=np.vstack([pred_mean - pred_lo, pred_hi - pred_mean]),

fmt="o-",

color="C0",

label="predictive for new unit (94% interval)",

)

ax.axhline(0, color="grey", lw=0.5)

ax.set_xlabel("weeks since launch")

ax.set_ylabel("effect")

ax.set_title("Event-study: population predictive for a new product")

ax.legend()

plt.show()

Placebo (lead/lag) model#

DGP: we generate two panels from the same random seed (so the noise, covariates and launch weeks are identical) but with different treatment effects:

With anticipation — the ramp/peak/decay post-launch curve plus a deliberate pre-launch linear build-up over the 8 weeks before launch (e.g. a pre-order period). The placebo bins in

[-8, -4)and[-4, 0)should absorb this and the automatic check should fail.Without anticipation — the same post-launch dynamics but strictly zero before launch. The placebo bins should be indistinguishable from zero and the check should pass.

Because the only difference between the two panels is the anticipation component, the contrast isolates exactly what the placebo test is designed to detect.

def anticipation_effect(tau, i, rng):

"""Dynamic post-launch effect + pre-launch build-up over 8 weeks."""

post = _amp_i[i] * launch_shape(tau)

tau_arr = np.asarray(tau, dtype=float)

lead = np.where(

(tau_arr >= -8) & (tau_arr < 0),

_amp_i[i] * 0.4 * (tau_arr + 8) / 8.0, # linear ramp up to ~40% of amp

0.0,

)

return post + lead

def clean_dynamic_effect(tau, i, rng):

"""Same post-launch dynamics, but strictly zero before launch."""

return _amp_i[i] * launch_shape(tau)

# Same seed → identical noise; only difference is the anticipation component

df_placebo_bad = simulate_panel(anticipation_effect, seed=2)

df_placebo_clean = simulate_panel(clean_dynamic_effect, seed=2)

def make_placebo_model():

return HierarchicalLaunchITS(

sample_kwargs={

"draws": 1000,

"tune": 1500,

"chains": 4,

"target_accept": 0.97,

"random_seed": 42,

"progressbar": False,

}

)

placebo_kwargs = {

"formula": "sales ~ 0 + emails + price",

"unit_col": "product",

"time_col": "week_idx",

"treatment_time_col": "launch_week",

"effect_type": "placebo",

"bin_edges": [0, 4, 8, 12, 16, 20, 26, 39, 52, 78, 10000],

"placebo_edges": [-26, -20, -16, -12, -8, -4, 0],

"seasonality": {"period": 52, "K": 2},

}

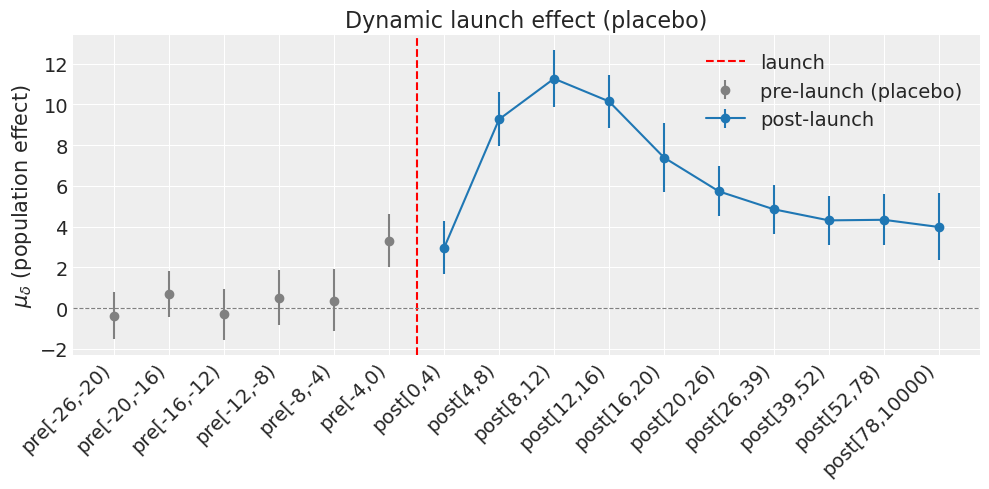

print("=== Panel WITH anticipation (placebo check should FAIL) ===")

result_placebo_bad = cp.HierarchicalInterruptedTimeSeries(

data=df_placebo_bad, model=make_placebo_model(), **placebo_kwargs

)

result_placebo_bad.summary()

result_placebo_bad.plot();

=== Panel WITH anticipation (placebo check should FAIL) ===

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [mu_alpha, sigma_alpha, z_alpha, mu_gamma, sigma_gamma, z_gamma, mu_beta, sigma_beta, z_beta, beta_season, mu_delta, sigma_delta, z_delta, sigma]

Sampling 4 chains for 1_500 tune and 1_000 draw iterations (6_000 + 4_000 draws total) took 573 seconds.

The rhat statistic is larger than 1.01 for some parameters. This indicates problems during sampling. See https://arxiv.org/abs/1903.08008 for details

Sampling: [beta_season, mu_alpha, mu_beta, mu_delta, mu_gamma, sigma, sigma_alpha, sigma_beta, sigma_delta, sigma_gamma, y_hat, z_alpha, z_beta, z_delta, z_gamma]

Sampling: [y_hat]

Sampling: [y_hat]

Sampling: [y_hat]

Hierarchical ITS (launch / event-study)

Formula: sales ~ 0 + emails + price

Effect type: placebo

Units: 15

pre[-26,-20) mu_delta = -0.364

pre[-20,-16) mu_delta = +0.684

pre[-16,-12) mu_delta = -0.296

pre[-12,-8) mu_delta = +0.515

pre[-8,-4) mu_delta = +0.365

pre[-4,0) mu_delta = +3.32

post[0,4) mu_delta = +2.96

post[4,8) mu_delta = +9.27

post[8,12) mu_delta = +11.3

post[12,16) mu_delta = +10.2

post[16,20) mu_delta = +7.4

post[20,26) mu_delta = +5.73

post[26,39) mu_delta = +4.85

post[39,52) mu_delta = +4.31

post[52,78) mu_delta = +4.34

post[78,10000) mu_delta = +3.99

Placebo check: FAIL (5/6 pre-launch bins contain 0 within the 94% HDI)

/Users/nathanielforde/Documents/Github/CausalPy/causalpy/experiments/hierarchical_interrupted_time_series.py:668: UserWarning: The figure layout has changed to tight

fig.tight_layout()

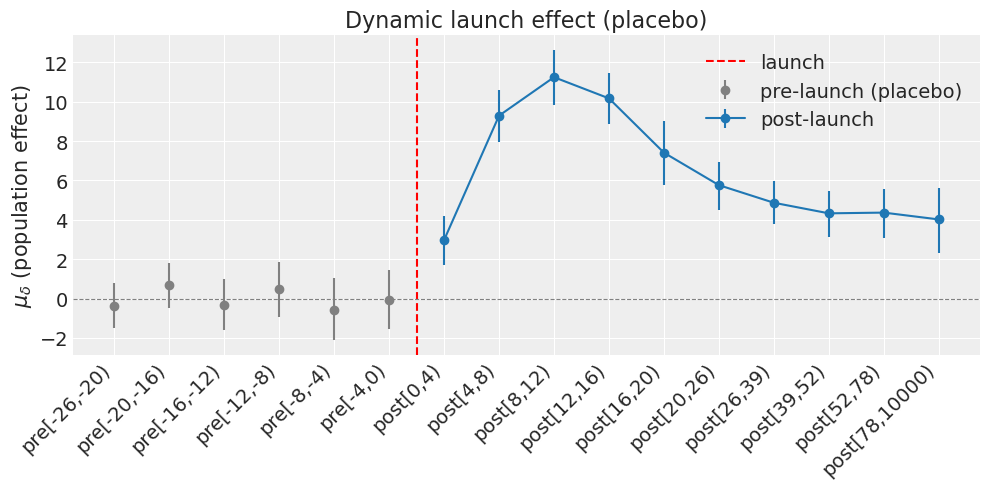

print("=== Same noise, NO anticipation (placebo check should PASS) ===")

result_placebo_ok = cp.HierarchicalInterruptedTimeSeries(

data=df_placebo_clean, model=make_placebo_model(), **placebo_kwargs

)

result_placebo_ok.summary()

result_placebo_ok.plot();

=== Same noise, NO anticipation (placebo check should PASS) ===

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [mu_alpha, sigma_alpha, z_alpha, mu_gamma, sigma_gamma, z_gamma, mu_beta, sigma_beta, z_beta, beta_season, mu_delta, sigma_delta, z_delta, sigma]

Sampling 4 chains for 1_500 tune and 1_000 draw iterations (6_000 + 4_000 draws total) took 600 seconds.

The effective sample size per chain is smaller than 100 for some parameters. A higher number is needed for reliable rhat and ess computation. See https://arxiv.org/abs/1903.08008 for details

Sampling: [beta_season, mu_alpha, mu_beta, mu_delta, mu_gamma, sigma, sigma_alpha, sigma_beta, sigma_delta, sigma_gamma, y_hat, z_alpha, z_beta, z_delta, z_gamma]

Sampling: [y_hat]

Sampling: [y_hat]

Sampling: [y_hat]

Hierarchical ITS (launch / event-study)

Formula: sales ~ 0 + emails + price

Effect type: placebo

Units: 15

pre[-26,-20) mu_delta = -0.377

pre[-20,-16) mu_delta = +0.673

pre[-16,-12) mu_delta = -0.311

pre[-12,-8) mu_delta = +0.494

pre[-8,-4) mu_delta = -0.56

pre[-4,0) mu_delta = -0.0915

post[0,4) mu_delta = +2.97

post[4,8) mu_delta = +9.29

post[8,12) mu_delta = +11.2

post[12,16) mu_delta = +10.2

post[16,20) mu_delta = +7.41

post[20,26) mu_delta = +5.76

post[26,39) mu_delta = +4.86

post[39,52) mu_delta = +4.33

post[52,78) mu_delta = +4.36

post[78,10000) mu_delta = +4.02

Placebo check: PASS (6/6 pre-launch bins contain 0 within the 94% HDI)

/Users/nathanielforde/Documents/Github/CausalPy/causalpy/experiments/hierarchical_interrupted_time_series.py:668: UserWarning: The figure layout has changed to tight

fig.tight_layout()

Model diagnostics#

The underlying HierarchicalLaunchITS is a standard PyMC model, so we can use pm.model_to_graphviz to visualise the DAG, ArviZ trace plots to check convergence, and az.summary for R-hat / ESS diagnostics. These are essential sanity checks before trusting the causal estimates.

Model graph — the plate diagram shows the hierarchical structure: population hyperparameters at the top, per-unit parameters inside the “unit” plate, and the likelihood at the bottom.

pm.model_to_graphviz(result_placebo_ok.model)

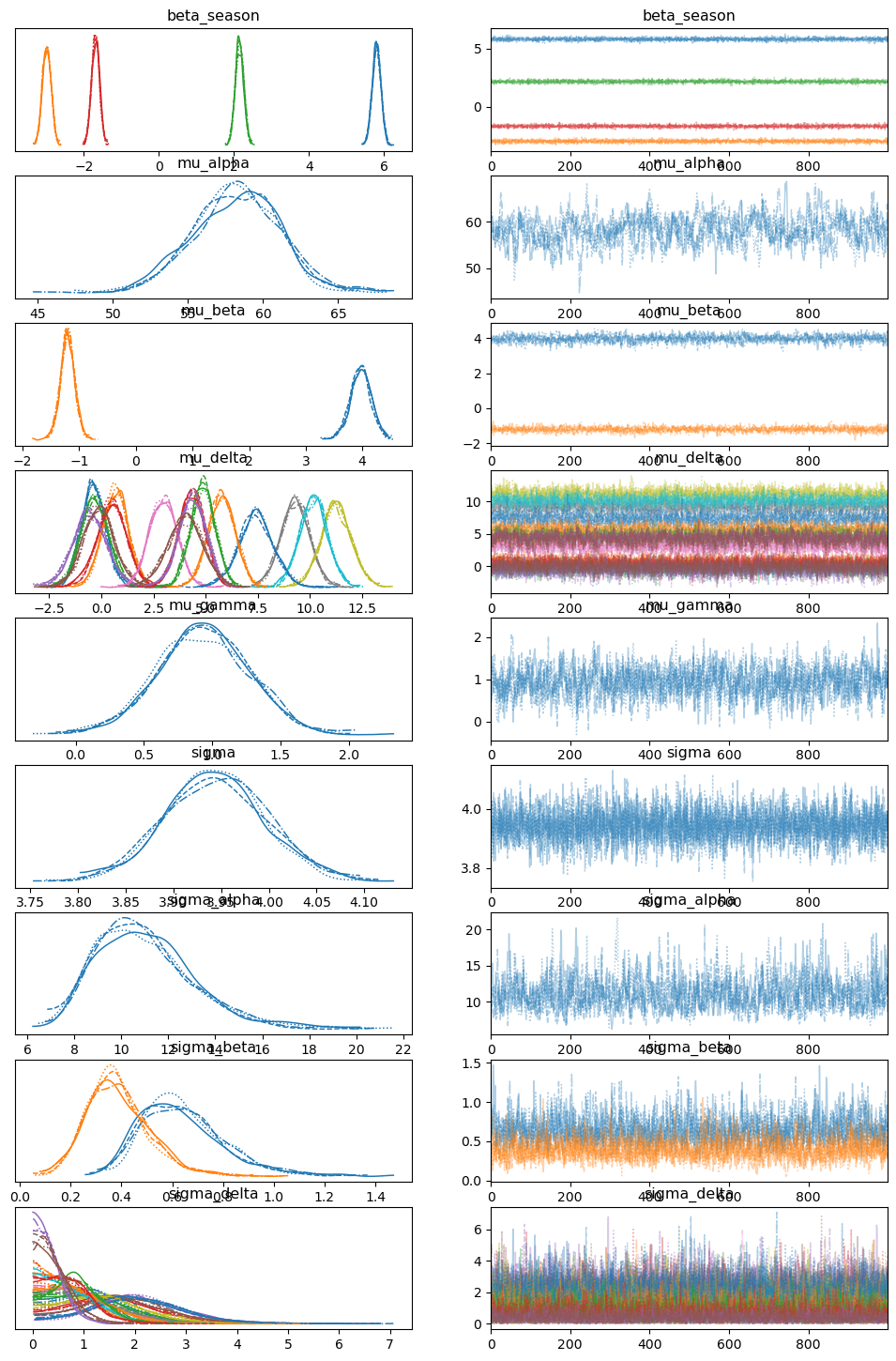

Trace plots — each row shows a population-level hyperparameter. Look for: chains that overlap and appear stationary (good mixing), no sustained trends, and no divergences flagged in the sampling output. The right-hand marginal posteriors should be smooth and unimodal.

import arviz as az

az.plot_trace(

result_placebo_ok.idata,

var_names=[

"beta_season",

"mu_alpha",

"mu_beta",

"mu_delta",

"mu_gamma",

"sigma",

"sigma_alpha",

"sigma_beta",

"sigma_delta",

],

)

plt.show()

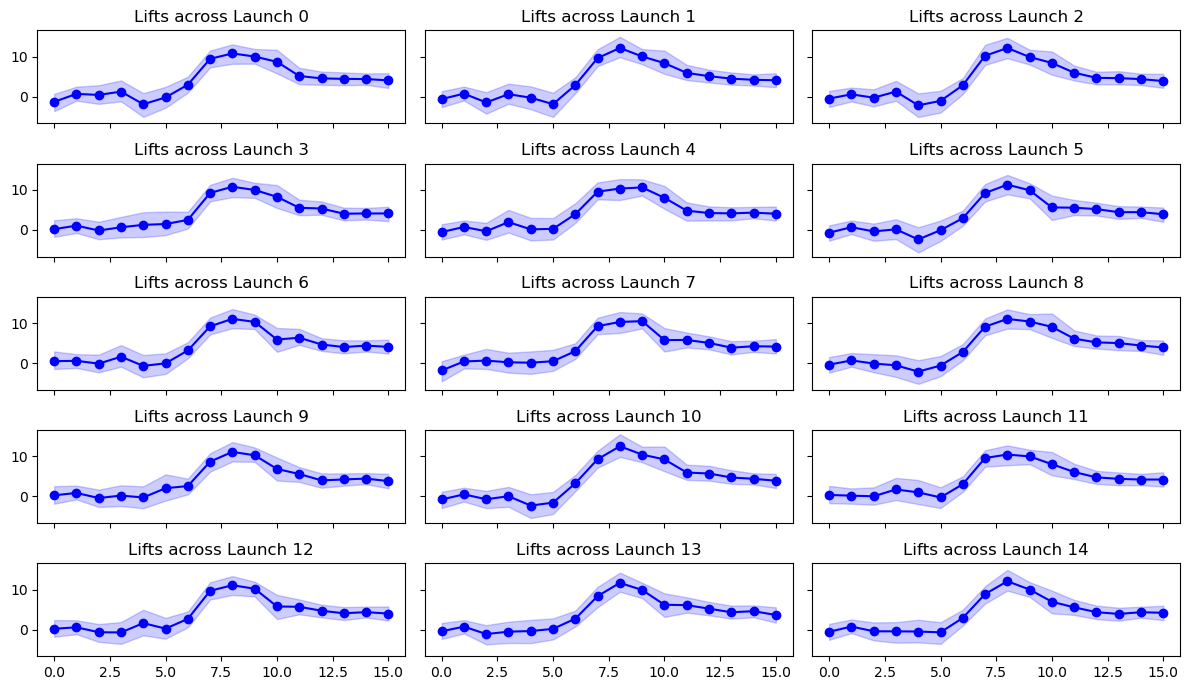

Per-unit effect profiles — each panel below shows one product’s posterior delta coefficients across the 16 event-time bins (6 pre-launch placebos + 10 post-launch).

fig, axs = plt.subplots(5, 3, figsize=(12, 7), sharex=True, sharey=True)

axs = axs.flatten()

summary_delta = az.summary(result_placebo_ok.idata, var_names=["delta"], hdi_prob=0.94)

summary_delta["index_col"] = summary_delta.index

summary_delta["index_col"] = summary_delta["index_col"].str.split("delta\[").str[1]

summary_delta["index_col"] = (

summary_delta["index_col"].str.split(",").str[0].astype(int)

)

for i, ax in enumerate(axs):

row = summary_delta[summary_delta["index_col"] == i]

ax.plot(range(16), row["mean"], marker="o", ls="-", color="blue")

ax.fill_between(range(16), row["hdi_3%"], row["hdi_97%"], color="blue", alpha=0.2)

ax.set_title(f"Lifts across Launch {i}")

plt.tight_layout()

AR(1) residuals (optional)#

Time series residuals are rarely i.i.d. When autocorrelation is present, the default Normal noise can produce overconfident uncertainty intervals. Passing ar_residuals=True adds a hierarchical AR(1) process to the residuals, implemented via pytensor.scan:

The tanh link ensures stationarity (\(|\rho_i| < 1\)). This requires a balanced panel (all units observed at the same time steps).

result_ar = cp.HierarchicalInterruptedTimeSeries(

data=df_instant,

formula="sales ~ 0 + emails + price",

unit_col="product",

time_col="week_idx",

treatment_time_col="launch_week",

effect_type="instant",

seasonality={"period": 52, "K": 2},

ar_residuals=True,

model=HierarchicalLaunchITS(

sample_kwargs={

"draws": 1000,

"tune": 1500,

"chains": 4,

"target_accept": 0.95,

"random_seed": 42,

"progressbar": False,

}

),

)

result_ar.summary()

result_ar.plot();

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [mu_alpha, sigma_alpha, z_alpha, mu_gamma, sigma_gamma, z_gamma, mu_beta, sigma_beta, z_beta, beta_season, mu_lift, sigma_lift, z_lift, mu_rho, sigma_rho, z_rho, z_ar, sigma_ar, sigma]

Sampling 4 chains for 1_500 tune and 1_000 draw iterations (6_000 + 4_000 draws total) took 377 seconds.

The rhat statistic is larger than 1.01 for some parameters. This indicates problems during sampling. See https://arxiv.org/abs/1903.08008 for details

The effective sample size per chain is smaller than 100 for some parameters. A higher number is needed for reliable rhat and ess computation. See https://arxiv.org/abs/1903.08008 for details

Sampling: [beta_season, mu_alpha, mu_beta, mu_gamma, mu_lift, mu_rho, sigma, sigma_alpha, sigma_ar, sigma_beta, sigma_gamma, sigma_lift, sigma_rho, y_hat, z_alpha, z_ar, z_beta, z_gamma, z_lift, z_rho]

Sampling: [y_hat]

Sampling: [y_hat]

Sampling: [y_hat]

Hierarchical ITS (launch / event-study)

Formula: sales ~ 0 + emails + price

Effect type: instant

Units: 15

E[mu_lift] = 11.3 E[sigma_lift] = 2.61

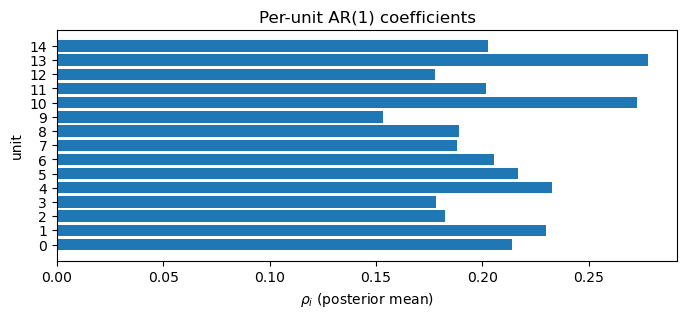

post_ar = result_ar.model.idata.posterior

rho_mean = post_ar["rho"].mean(("chain", "draw")).values

fig, ax = plt.subplots(figsize=(8, 3))

ax.barh(range(len(rho_mean)), rho_mean)

ax.set_yticks(range(len(rho_mean)))

ax.set_xlabel(r"$\rho_i$ (posterior mean)")

ax.set_ylabel("unit")

ax.set_title("Per-unit AR(1) coefficients")

ax.axvline(0, color="grey", lw=0.5)

plt.show()

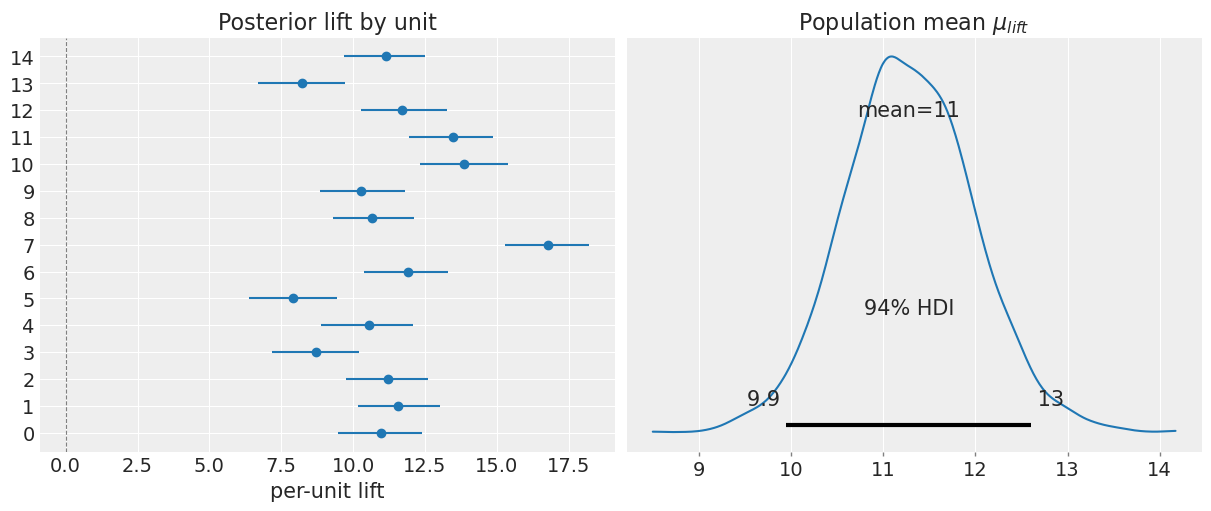

result_ar.plot_unit(unit_id=6)

plt.show()

Notes on the implementation#

All hierarchical parameters use a non-centered parametrization for sampler health.

Hierarchical linear time trends \(\gamma_i \sim \mathcal{N}(\mu_\gamma, \sigma_\gamma)\) are always included, allowing each unit’s baseline to drift linearly over time. The time index is standardized internally for numerical stability.

Saturation (

effect_type='saturation') replaces the instant level shift with a Hill curve, \(\text{effect}_i(\tau) = L_i \, \tau^s / (k_i^s + \tau^s)\). The ceiling lift \(L_i\) and half-saturation time \(k_i\) are hierarchical per unit (log scale, non-centered); the Hill exponent \(s\) is a single shared population parameter.mu_logk/sigma_logk/suse fixed, generic priors (not data-adaptive totime_col’s scale) — override them viapriors=if your time index isn’t in “a handful of periods to ramp up” units, e.g. daily rather than weekly data.Optional AR(1) residuals (

ar_residuals=True) add per-unit autocorrelated noise viapytensor.scan. The AR coefficient is constrained to \((-1, 1)\) via atanhlink and partially pooled across units. Requires a balanced panel.Priors on population-level scale parameters are derived from the data via

priors_from_dataso the model is approximately scale-invariant.Covariates from the patsy formula are standardized internally; the hierarchical \(\alpha\) takes the place of an intercept (you should not include one in

formula).print_coefficients()also reports covariate coefficients back on their original (unstandardized) scale.Any prior can be overridden via the

priors=argument toHierarchicalLaunchITSusing thepymc_extras.prior.Priorsystem.